- Weekly Wizdom

- Posts

- Monthly Report: May 2024

Monthly Report: May 2024

Wizard of Soho

June 02, 2024 • Estimated Reading Time: 15 minutes

Housing Market

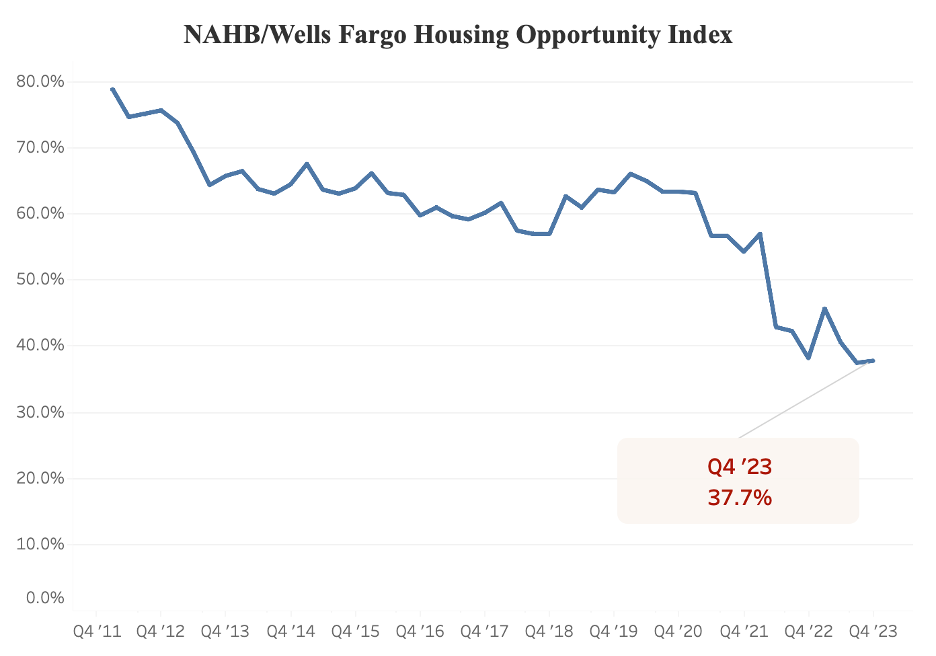

Across the housing market, there continues to be mixed data that is undermining the overall arching struggling industry. To back this statement, building permits fell significantly while housing increased. One reason for the decline in permits would be increased construction costs. However, housing starts would increase due to previous permits that were pulled in optimistic ideas of costs possibly moving lower with falling inflation. However, we have yet to see this come down in construction. Despite this, around 66% of families prefer new construction over existing homes. Similarly, new home sales dropped even further than existing home sales, primarily due to how unaffordable it has become to buy a house.

NAHB, 2024

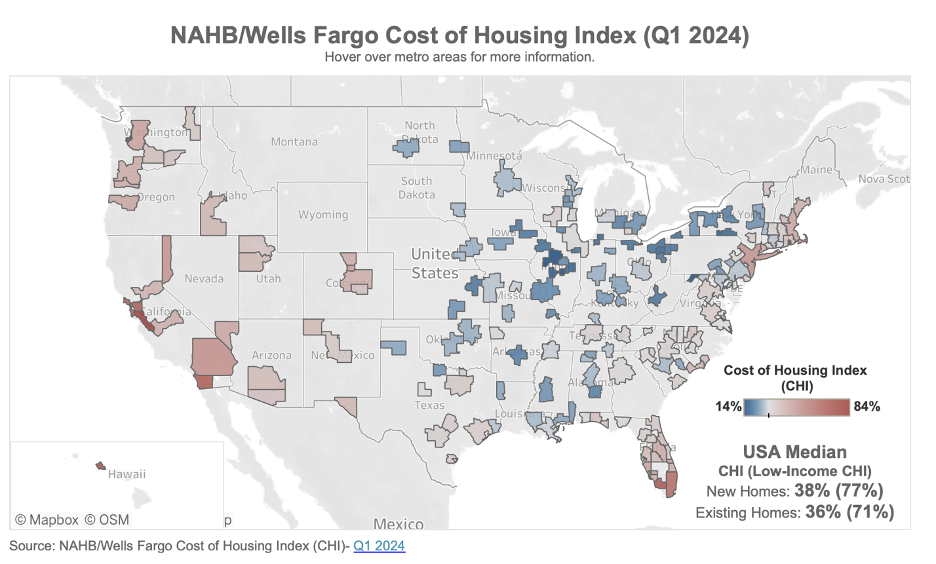

The regions where this continues to be a problem are, not shockingly, the coasts. Most of the Midwest has remained more affordable, so we have seen more demand in those regions. However, the increased influx of people into these regions to evade higher construction costs has now oversaturated the market. Over the last few years, many hot markets, such as Austin, Milwaukee, and Raleigh, have moved into more unfordable territory. Around 60% of median-income earners spend more than 50% of their income on a home in these markets.

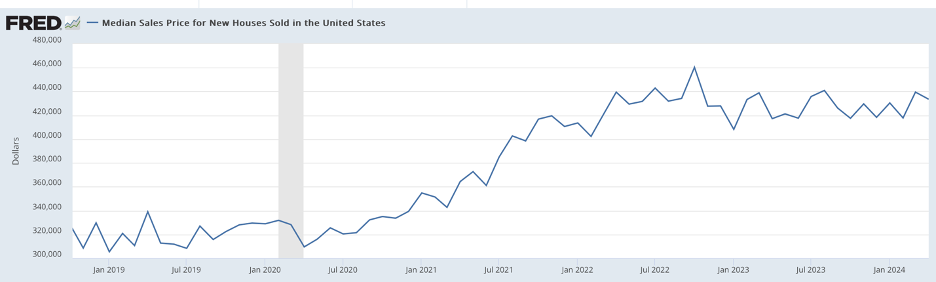

Housing production and a lack of demand in the new-home market have created an overabundance. That has been the case for the last two years; the result is that new construction has been a much more affordable option than existing homes. Prices have been mostly steady over that same time when supply has outpaced demand. This trend is expected to continue for quite some time now, as rates will not likely come down anytime soon.

NAHB, 2024

Fred, 2024

International

United Kingdom news for the housing market has been much of the same as the US, as interest rates have been kept at their previous levels. Nationwide housing prices dropped MoM but increased YoY. PMI increased, so there continues to be mixed data.

Canada has also reported very mixed results. The new housing price index was mostly flat but increased Month over Month. The total number of housing starts dropped drastically for April.

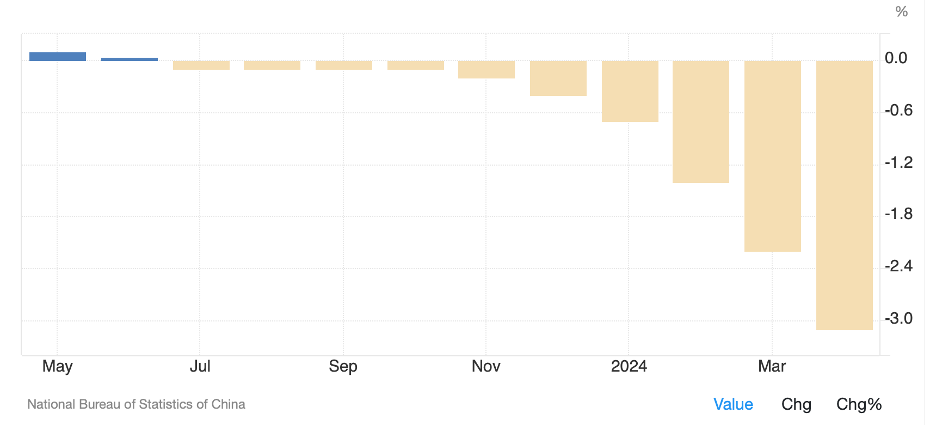

China news is nothing has changed outside of the continuing pending housing crisis. Housing prices dropped yet another large percentage for the 10th month. This has been in the news for a while, and the Chinese government has attempted to elevate the issue. But, so far, the Chinese people have been let down since the country has been involved in trading wars with the world for the last decade.

Fixed Income Markets

Yield Curve

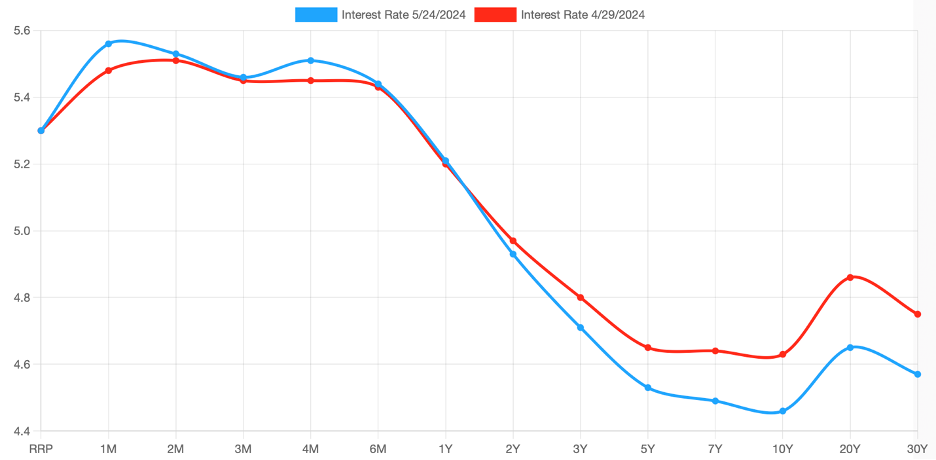

Rates mainly remained unchanged for the last month. The latest Fed meeting showed that inflation stayed sticky and that much more work would need to be done. With the market setting new all-time highs, there is more emphasis on higher rates for longer. Some recent data on the labor market showed that fewer jobs are available, and hiring has slowed. The unemployment rate increased while wages also dropped. Jobless claims spiked in the first week of May but quickly came down, in what could have been a blip in the data. Nonetheless, the labor market is starting to show some cracks that could give early signs of a recession.

US Treasuries Yield Curve, 2024

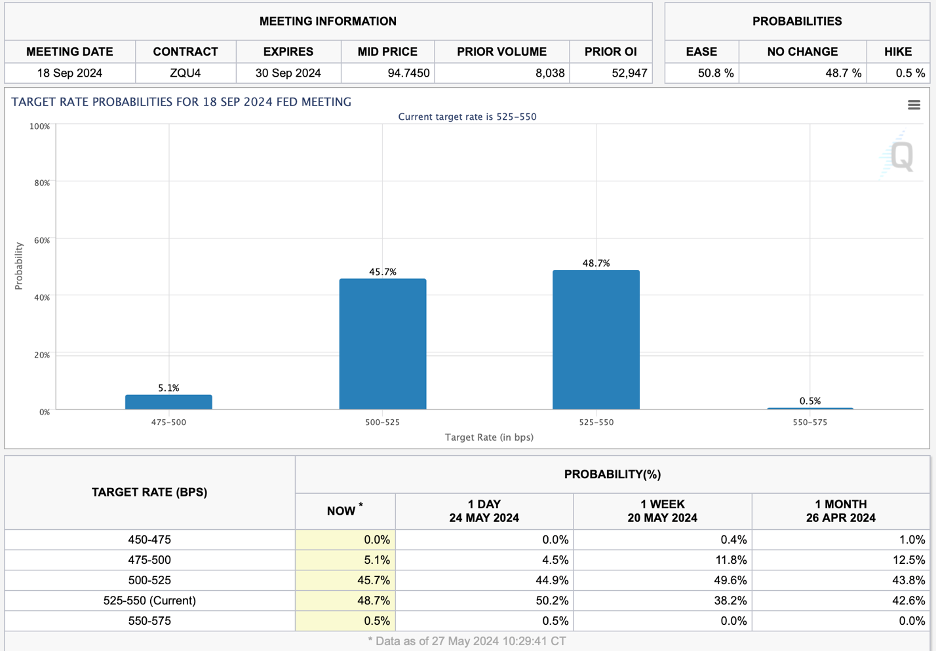

Because of the recently mentioned stick inflation, rates must remain higher for longer. As shown below, the most recent meeting with a possible rate cut would be by September. Even the Fed has mentioned that this might not be possible and that it could be until the end of the year before we see a rate cut. The expectations have now dropped to 2.5 cuts before the end of the year, which initially started at seven cuts. Even this is wishful thinking, as inflation has still stayed at elevated levels above the Feds target. However, if the labor market started unraveling, we could see a cut soon. One thing to consider is that inflationary prices will increase by moving away from cheap imports from countries like China and towards more domestic materials. Potentially, towards 3% YoY if trade were to be significantly cut.

CME Group, 2024

Investment-grade/Junk Bonds and Corporate Bonds

Credit spreads continue to go towards some of the lowest levels we have seen. Jamie Dimon even mentioned that these are unsustainable and should most likely expand in the future. When we see this, more times than not, we see an economic slowdown and, depending on the rate of expansion, a recession.

Fred, 2024

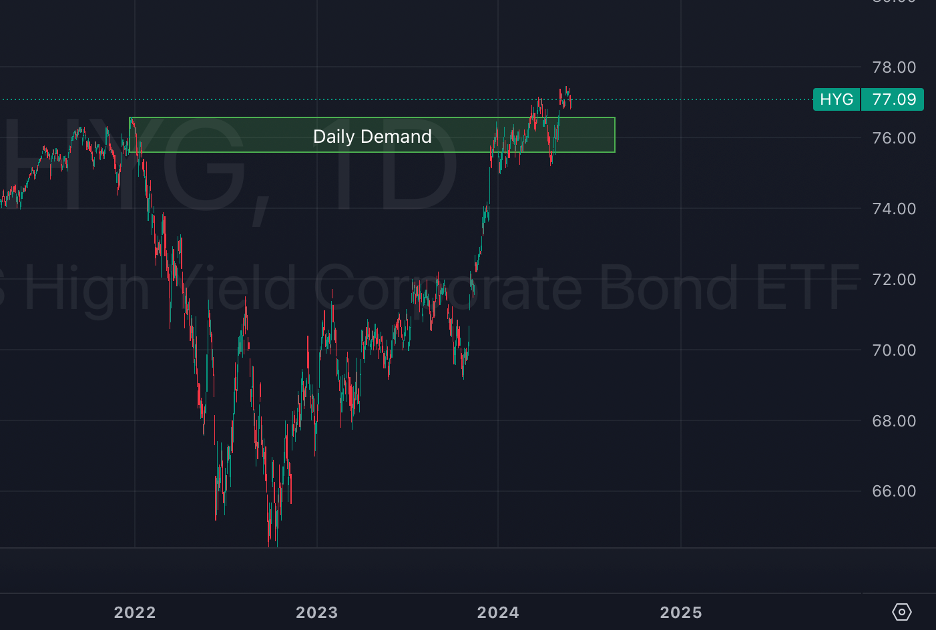

Bonds have had a slow start to the year, once again, and continue to be range-bound. Investment grade bonds have been slowly moving down, but with the last monthly move down in back-end rates, the bond prices have moved up slightly. Similarly, with HYG bonds, there has been a consistent upward move, as they have provided higher yields. Many people are now moving away from bonds, as the equity premium rate is the lowest it has ever been in many years, which means that people are being paid to take risks or not having to offer up much to take risks.

Tradingview, 2023; Investment Grade Bonds (LQD)

Tradingview, 2023; High Yield Bonds (HYG)

Interestingly, TLT moved up based on what was mentioned before and bounced off this region. That is a very bearish sign, suggesting more room for the downside. I agree with this on a macro level because rates should stay higher for longer, raising back-end rates.

Tradingview, 2023; TLT

Oil & Commodities

Crude

Brent is around its three-month lows, trading around $82, while the difference with WTI has narrowed the most in the current year.

Short-Term Fundamentals

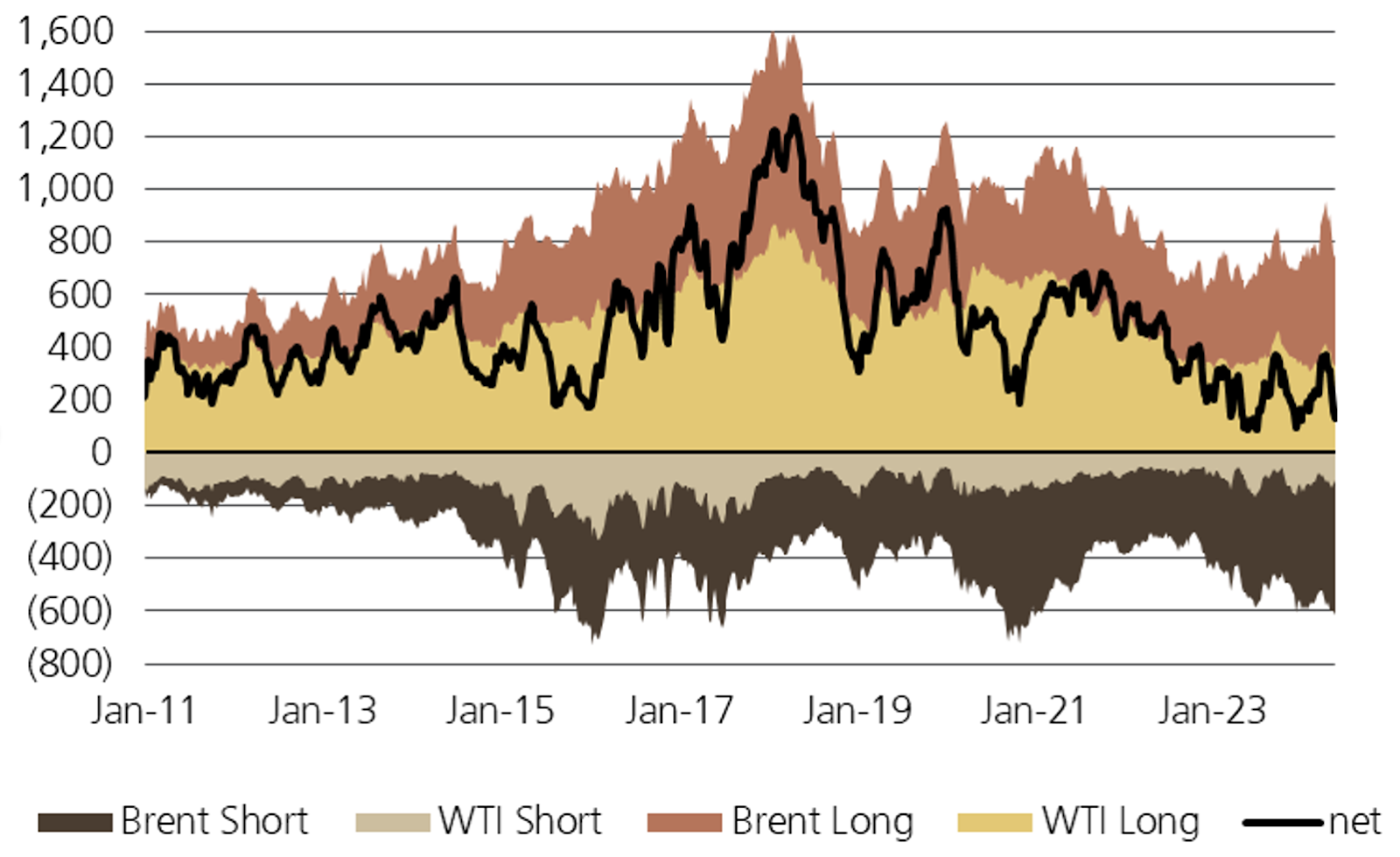

Positioning

As the chart above shows, positioning is very thin now, with overall length across Brent and WTI flirting with the lowest on record since 2011.

Last week, speculators were sellers of crude and built up the largest short position since December.

Stocks

US stock levels continue to follow a typical seasonal pattern of builds, while European builds are getting stronger. In contrast, Singaporean inventories are drawing, mainly because of fuel oil and the increased demand for shipping.

China’s lower refinery runs in recent months have supported rebuilding the country’s onshore crude inventories, rising for the third consecutive month to 1.06bb.

Floating Storage

Floating storage remains somewhat stable with 5-10m barrel draws/builds each week, mainly from Asia.

Physical Market

CFDs in Europe are coming under pressure, with the front spreads in contango highlighting the recent weakness in crude.

Assessments of WTI grades are also in contango, with July loading periods having higher prices than June, which is usually a sign that the market is well supplied.

Refinery Runs

Crude’s underperformance has mainly been attributed to lower run rates globally, as maintenance season in areas such as China and weak margins across the globe cause crude appetite to drop. In the last few weeks, all main cracks (gasoline, diesel, and 0.5% fuel) have plummeted, eroding the refinery margins (especially in Asia). We should see more crude buying as Asia moves outside the maintenance season.

Manufacturing

Japan’s manufacturing is back into growth, printing higher than 50 after 1 year,

In the US, the Fed’s regional manufacturing index experienced a pullback this month as new orders dipped into contraction territory.

OPEC

Most analysts expect OPEC+ members to continue with the voluntary cut of 2.2m barrels, which is supposed to expire in June.

The voluntary cut, introduced in November 2023, adds to the already 3.6mn bpd of cuts that reduced the group’s crude output by about 5.8mn barrels daily, or about 5 percent of global supply.

Freight: Trade Idea

Container freight prices are now 50% higher than before the Israel/Palestine conflict.

Without the conflict being resolved, the shipping situation would remain unstable.

With the fleet used for Russian products and the already large journeys performed, we can expect freight rates to also rise for tankers.

In recent weeks, India has been using dirty tankers to transfer diesel. However, with stockpiles of diesel increasing globally and demand being limited, this will likely reverse in the coming weeks. That would create a good opportunity to get long, clean, wet freight as ship supply will come down, and the situation with L1s and L2s remains tight in the Middle East. Enforcing this, the Middle East also comes back from maintenance, meaning higher demand for ships to export products in a few weeks.

Russia

The graph below from Platts shows all the Refineries in Russia that are within range of Ukrainian drones. A total of 4.8m barrels per day are within range.

Other News

India has asked private refiners such as Reliance for help locking deals for at least one-third of its crude supply with Russia at a fixed discount.

The Buzzard oilfield in the North Sea is experiencing a temporary production outage. There is no information on when the outage started or how long it will last.

Buzzard, one of the largest producing UK fields, is linked to the Forties crude stream, one of the North Sea crude grades that underpins Brent. The Forties crude stream will load seven cargoes of 700,000 barrels each in June. Two of these will be delayed because of the outage.

According to Reuters, Saudi Aramco may cut prices for most crude grades it sells to Asia in July. If true, this would be the first cut in five months.

Iran has signed deals worth $13bn to increase oil output by 350,000 bpd by next year.

China continues to import Iranian oil disguised as Malaysian oil, and the overall enforceability of sanctions on Iran has been limited as attention has been paid to Russian barrels.

NOAA forecasts an 85% chance of above-normal Atlantic hurricane season. Typically, this causes refineries to close down, meaning less demand for crude and less gasoline supply.

China

Beijing is mulling a proposal to have local governments buy millions of unsold homes nationwide.

Under the preliminary plan, state-owned enterprises would be asked to help purchase the homes from distressed developers at steep discounts using loans provided by state banks.

It is an ambitious proposal that Jefferies estimates would cost at least 2 trillion yuan ($277 billion).

Xing Zhaopeng at Australia & New Zealand Banking Group said the boost to GDP could be as much as 1 percentage point. That gives the Chinese government some breathing room as it strives to hit its annual growth target of about 5%.

Refined Products

Products have struggled a lot in the last month, with gasoline and jet holding better than diesel/gasoil (which is currently in contango), but overall, they have all cracked down for the last few weeks.

In the US, air travel data showed that domestic flights for May rose by 5% monthly and almost 6% yearly to slightly above 90 million, surpassing pre-covid levels. The number of air passengers in the US hit a post-pandemic high of around 2.95 million on May 24.

Most Northeast Asian refineries are set to restart operations in the coming weeks following planned maintenance. This should create further issues for the closed arbitrage into other regions such as Europe, keeping the product in Asia and weighting on cracks.

Preliminary calculations show that China’s implied refinery runs sunk to 14.4m bpd in May, the lowest since last July, as the country was under seasonal maintenance and domestic margins weren’t that attractive.

Other Commodities

NatGas

Some supply issues on the LNG side with:

OMV (Austrian company) said that gas supplies from Russia’s Gazprom could be suspended for legal reasons, reassuring that the supply will be diverted from elsewhere.

The power outage in Malaysia resulted in a loss of 250k of LNG.

Russia-Ukraine deal on gas.

Cocoa

Cocoa futures in New York saw the largest price drop in the last 60 years following a weather forecast for key producer countries showing more rainfall. This was for Ghana and the Ivory Coast, critical countries for cocoa production.

The big move was amplified by the high open interest in cocoa and long positioning as everyone looked to join the move that saw cocoa triple this year.

Copper

China has been stockpiling copper since the start of this year, and copper stockpiles have been at their highest level since 2020.

Usually, when China stockpiles, prices retreat in anticipation of when the buying will finish; however, we currently have both prices and China’s stockpiles increasing simultaneously.

US officials have highlighted the option of creating a strategic reserve of Copper Cathode in the US, potentially in response to the stockpiling of refined copper seen in China.

The reasoning is speculated to concern supply chains for EVs, solar panels, data centers, and the overall property market.

References

(n.d.). US Treasuries Yield Curve. US Treasuries Yield Curve. https://www.ustreasuryyieldcurve.com/

(n.d.). CME FedWatch Tool. CME Group. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

(n.d.).Trading Economics. Trading Economics. https://tradingeconomics.com/united-states/nahb-housing-market-index

(n.d.).Goldman Sachs. Goldman Sachs. https://www.goldmansachs.com/

(n.d.).Bloomberg. Bloomberg. https://www.bloomberg.com

Disclaimer

Wizard of Soho LLC and Weekly Wizdom publish financial information based on research and opinion. We are not investment advisors, and we do not provide personalized, individualized, or tailored investment advice, nor do we provide legal advice or information. The publisher does not guarantee the accuracy of the information provided on this page. All statements and expressions present are based on the author's or paid advertiser's opinion and research. Directly or indirectly, no opinion is an offer or solicitation to buy or sell the securities or financial instruments mentioned.

As news is ever-changing, the opinions included should not be taken as specific advice on the merits of any investment decision. Investors should pursue their investigation and review of publicly available information to make decisions regarding the prospects of any company discussed. Any projections, market outlooks, or estimates herein are forward-looking and inherently unreliable. They are based on assumptions and should not be construed to be indicative of actual events that will occur.

Contrarily, other events that were not considered may occur and significantly affect the returns or performance of the securities discussed herein. The information provided is based on matters as they exist on the date of preparation and do not consider future dates. As a result, the publisher undertakes no obligation to correct, update, or revise the material in this document or provide any additional information. The publisher, its affiliates, and clients may currently or foreseeably have long or short positions in the securities of the companies mentioned herein. They may, therefore, profit from fluctuations in the trading price of the securities. There is, however, no guarantee that such persons will maintain these positions. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile, or any other means is illegal and punishable.

Neither the publisher nor its affiliates accept any liability for any direct or consequential loss arising from any use of the information contained herein. By using the website or any affiliated social media account, you consent and agree to this disclaimer and our terms of use.