- Weekly Wizdom

- Posts

- Monthly Report: June 2024

Monthly Report: June 2024

Wizard of Soho

July 01, 2024 • Estimated Reading Time: 16 minutes

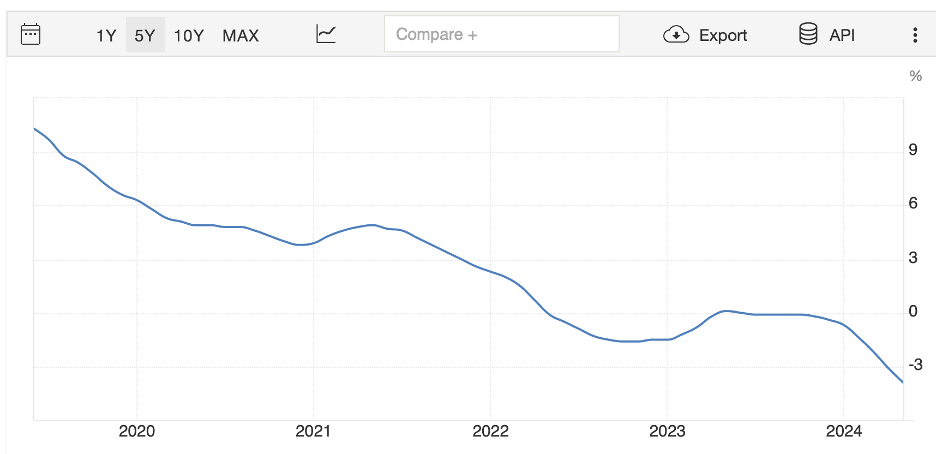

Housing Market

The June housing market indicates a turning point, suggesting potential challenges ahead. This trend is evident in various sectors, particularly multifamily properties, and is becoming apparent in the single-family housing market. A sustained slowdown was anticipated, but prolonged high interest rates could significantly impact this region. Homebuyers have been turning to new construction to avoid steep prices due to the shortage of existing homes. However, this negatively impacts consumers as material costs remain elevated, leading to higher home prices.

A key observation was the rising preference for suburban and rural properties, which gained momentum during the pandemic and continued as remote work arrangements became more permanent. This led to a surge in new home construction in these areas, driven by the demand for larger living spaces and more affordable housing options. Urban markets experienced slower price growth than their suburban and rural counterparts due to the higher costs associated with urban living and the enduring impact of the pandemic on city lifestyles.

Eye on Housing, 2024

The sentiment index and housing starts both experienced declines despite the shift in longer-term mortgage rates toward more affordable levels. The decrease in housing starts and permits indicates a slowdown in the market and reflects the challenge of affording these higher rates. Additionally, there has been a drop in sentiment, further reinforcing this trend. With elevated rates and a supply shortage in existing single-family homes, housing prices have reached record highs.

Fred, 2024

International

Unsurprisingly, we've observed a surge in the housing market in countries implementing interest rate cuts. In the UK, housing prices and the construction Purchasing Managers' Index (PMI) show a consistent upward trend. The lower interest rates have resulted in increased market demand and inflated prices, a trend reflected in the data. We are beginning to witness similar patterns in countries such as Sweden, Switzerland, and Canada, all of which made rate cuts preceding the Federal Reserve. Notably, Canada experienced a slight increase in housing prices and a significant rise in new housing starts.

China's housing market showed improvement in June, particularly in major cities like Beijing, Shanghai, and Shenzhen. Government measures, such as relaxed lending policies and incentives for first-time homebuyers, contributed to this positive trend. However, challenges remain, including managing the significant inventory of unsold homes in smaller cities and addressing concerns about housing affordability. The market also saw growing interest in sustainable and energy-efficient housing solutions, aligning with China's broader environmental goals and regulations. Overall, the housing market in China seemed poised for gradual growth, supported by policy interventions and shifting buyer preferences.

House Prices YoY, National Bureau of Statistics of China

Fixed Income Markets

Yield Curve

In the previous month, there was a significant decrease in the back-end rates, indicating potential instability in the US market. The labor market data, particularly the JOLTS job openings, revealed a notable increase after a prolonged decline. Despite the non-farm data showing higher-than-expected results, there has been a surge in the unemployment rate and claims. This trend aligns with historical patterns, as the inverted yield curve, which is currently in effect, typically leads to disruptions in the labor market about 16 months after its initial inversion. These disruptions are becoming evident, prompting the market to signal the need for more rate cuts to provide support.

Additionally, there are expectations for a considerable drop in GDP, indicating a cooling economy. Inflation has also been decreasing, as evidenced by declining housing starts and permits, signaling the effectiveness of qualitative tightening. However, some indications reversing these measures might be necessary to prevent adverse economic effects.

US Treasury Yield Curve, 2024

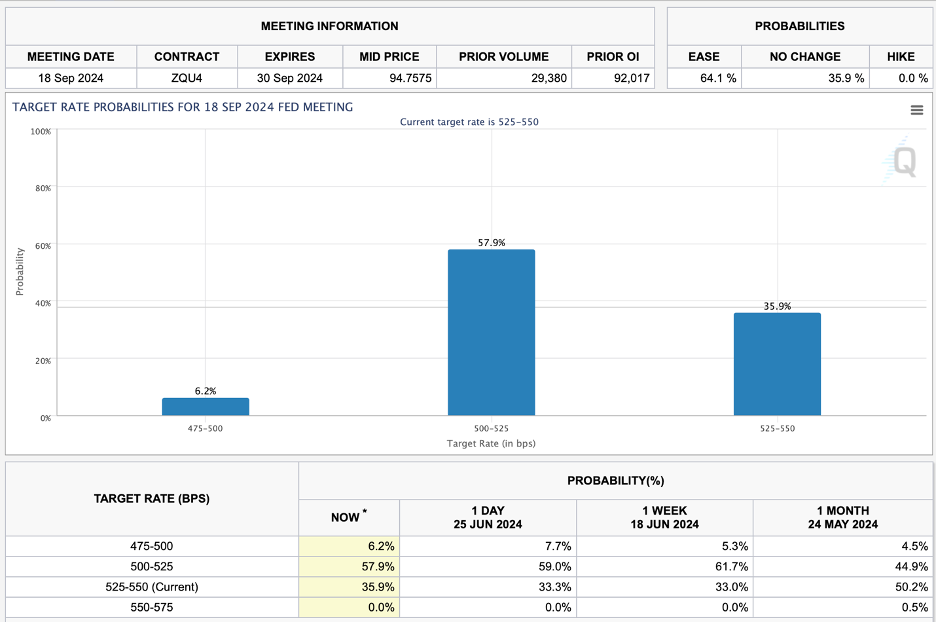

It is anticipated that the first interest rate cut will be implemented at the September meeting, with expectations of a total of 2.5 cuts before the year ends. Despite these market expectations, several Fed board members have emphasized the possibility of only one rate cut, given concerns about persistent inflationary pressures in certain sectors such as food away from home, transportation, and shelter. Recent actions by the ECB and BoC signal an early initiation of rate cuts, instilling optimism in the market about potential future cuts. However, the ECB has already halted its rate-cutting initiatives, possibly indicating underlying reservations about aggressive rate cuts. Notably, the recent rate hikes in the US have been historically rapid, and the Fed is cognizant of this trend. A 25 basis point reduction may have a limited impact on addressing the prevailing challenges. Maintaining higher interest rates until inflation stabilizes to more acceptable levels appears to be a prudent course of action.

CME Group, 2024

Investment-grade/Junk Bonds and Corporate Bonds

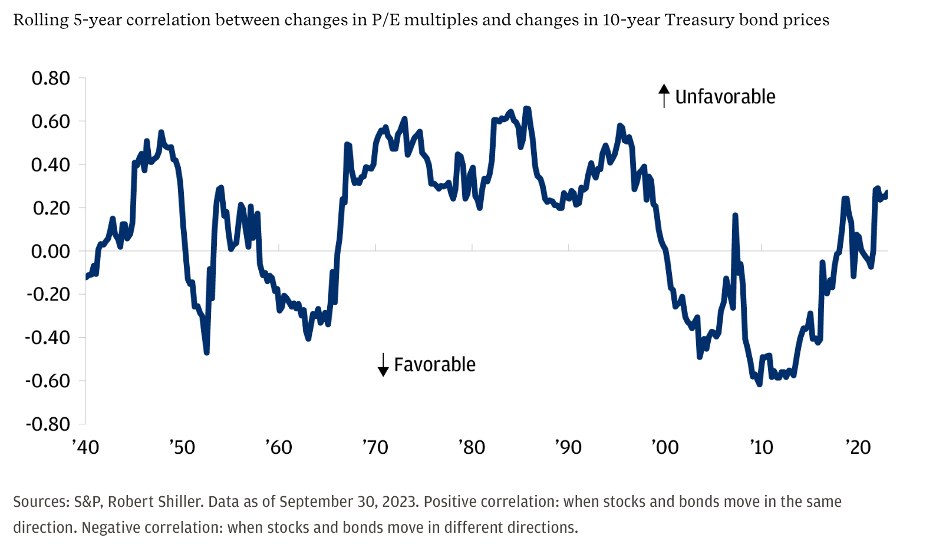

The persistently low credit spreads and range-bound bond performance are notable trends. Although historically low credit spreads can indicate an impending market crash, the market is reaching new highs. However, small caps and bonds are struggling, with bonds remaining range-bound as the market determines the direction of interest rates. Notably, longer-duration ETFs such as TLT have improved as back-end rates drop, but higher yields outperform while others struggle. This situation is problematic because bond and stock yields are becoming more correlated, challenging the typical 60% bonds and 40% stocks portfolio allocation strategy. Traditionally, this approach capitalized on the safety of bonds and the higher yield of stocks. Still, the high correlation has rendered this strategy ineffective due to rising rates and inflation and offers no refuge from speculation.

Tradingview, 2023; Investment Grade Bonds (LQD)

Tradingview, 2023; High Yield Bonds (HYG)

JP Morgan, 2023

Oil & Commodities

Crude

Crude has been rallying since the last OPEC+ meeting despite the intention to increase output towards the end of the year. The low positioning across the barrel, the revival of the physical market, improvements in global manufacturing, the seasonality of strong crude demand (China and Europe moving out of maintenance season), and the seasonal impacts of summer demand for flights and road travel have helped prop up this rally.

The main risks for the oil rally are the buildup of US crude in PADD3, the potential release of further oil from the SPR, and poor economic data from China.

Physical

Strong recovery in the physical market

Prompt DFL has been rallying hard the last few weeks (from -30 to 50 cents)

A healthy recovery in distillate cracks over the last few weeks may boost confidence even for complex margins, particularly in Europe and Asia.

Crude flows

Global crude supplies were almost 700,000 bpd higher in May, but total exports are still well below last year's peaks.

The main source of export growth, the Atlantic Basin, has been losing market share. This trend will likely continue as OPEC+ prepares to increase output in September. Under the most recent agreements, Saudi Arabia and UAE will be able to produce up to 1.5mbd more in the 12 months from September.

Stocks

US crude inventories are close to the long-term seasonal average. Stocks were just -2 million barrels below the prior 10-year seasonal average by mid-June, compared with a surplus of +15 million barrels at the same point in 2023. Inventories along the Gulf of Mexico (PADD 3) have climbed to their highest level for the time of year since 2020. Inventories were +25 million barrels above the prior ten-year seasonal average, up from a surplus of just +8 million barrels on March 19.

Europe's inventories have been rising even as seasonal refinery maintenance is underway, in contrast to global inventories, which have reversed their recent builds. As of early June, European crude inventories had increased to levels last seen around 18 months ago.

The major concern for Atlantic Basin producers will be how much crude will not be exported to Europe, especially now that maintenance season is over.

China’s drop in refinery runs in recent months has supported rebuilding the country’s inventories, which have risen for the third consecutive month to 1 billion barrels.

Positioning

Speculators have started building up net longs in recent weeks after a series of months of low positioning.

The combined position across all six contracts was in only the 6th percentile for all weeks since records started.

OPEC

OPEC⁺ has signaled an important shift from giving a lifeline to shale in 2023 to squeezing them in 2025.

OPEC+ on June 2 agreed to extend 3.66 million bpd of cuts by a year until the end of 2025, extend the latest cut of 2.2 million bpd until the end of September, and gradually phase it out over the course of a year from October.

The plan involves a gradual return of supply starting in October 2024 and extending through September 2025. Supply increments will be around 180,000 bpd each month during the fourth quarter of 2024 and approximately 200,000 bpd from January to September 2025.

Reminders

Official Cuts (October 2022)

Voluntary Cuts #1 (April 2023)

Voluntary Cuts #2 (latter half of 2023)

Russia's energy ministry said oil production in May exceeded quotas

Iraq's oil ministry said on Wednesday it is fully committed to compensating for any crude oil overproduction in 2024 throughout the compensation period, which will run until September 2025

SPR

The Biden administration is ready to release more oil from the SPR to limit any increases in gasoline prices, which would cause complaints before the US election in November.

According to the AAA motoring group, US petrol prices averaged $3.45 a gallon on Sunday. This was down slightly from a year ago but still more than 50 percent higher than when Trump was president.

In June, nationwide gasoline retail prices averaged $3.59 per gallon, which was close to the last century's average.

Russia sanctions

Denmark is considering ways to limit the shadow fleet of tankers from carrying Russian oil through the Baltic Sea.

Russia sends about a third of its seaborne oil exports, or 1.5% of global supply.

China

The delay in starting up Shandong’s Yulong refinery to at least Q4 this year confirms the bearish refinery margin story.

Vortexa’s calculations show that China’s implied refinery runs declined for the third month to 14.5mbd in May, the fourth consecutive decline year on year.

Crude stocks in other coastal areas remained flat. This suggests that Shandong teapots are still struggling with bearish refining margins, and their appetite will remain weak in the near term.

Current onshore crude stock, standing at 944mb in aboveground oil storage tanks as of 5 June, equates to 90 days of seaborne crude imports in 2023, indicating that further stockpiling is not urgent.

China added more than 1 million barrels per day (bpd) of crude oil to stockpiles in May as soft imports outweighed weaker refinery processing volumes. Up from 830,000 bpd in April, according to calculations based on official data.

The volume of crude processed by refiners was 14.25 million bpd, dropping from 14.30 million bpd in April to 14.60 million bpd in May last year.

Crude oil imports were 11.0 million bpd in the first five months of the year, down 130,000 bpd or 1.2% from the same period in 2023.

Refined Products

On the fuel side, gasoline and diesel inventories have been rising relative to the seasonal trend in the United States.

US refineries: Very high runs!

Refineries processed 17.5 million barrels per day of crude the previous week, the fastest seasonal rate since 2018.

Refineries employed 95% of their operable capacity, up from 94% last year and the highest percentage since 2019.The gross margin from turning 3 barrels of crude into 2 barrels of gasoline and 1 barrel of diesel, known as the 3-2-1 crack spread, has averaged $25 per barrel in June, down from $31 in March.

As a reminder, the 3:2:1 crack spread approximates the average yield at a typical U.S. refinery (for every three barrels of crude oil the refinery processes, it makes two barrels of gasoline and one barrel of distillate fuel).

Gasoline

Stocks were 1 million barrels above the prior 10-year seasonal average, erasing a deficit of 6 million barrels two months ago.

Most of the draws in Q1 came because of the outage at BP’s refinery at Whiting in Indiana following a site-wide electricity failure at the start of February.

Between late January and the middle of March, gasoline inventories were depleted by around 13 million barrels more than the seasonal average.

The high margins for producing gasoline and the very high runs in the US have created an oversupply of gasoline.

US traffic volumes have rebounded but remain well below the pre-pandemic trend. They are increasing well under 2% per year, which isn’t enough to cover the reduction in gasoline demand from ethanol blending, improvements in fuel efficiency, and demand for electric and hybrid vehicles.

Diesel

European gasoil spreads and cracks have been rallying in recent weeks, flipping the structure from contango to backwardation after two months.

At the same time, US diesel cracks traded above gasoline for a short time, which is unusual for this time of year.

US

The volume of distillate fuel oil supplied to the US domestic market was under 3.7 bpd in March 2024, the lowest for the time of year since 1998.

HO spreads and cracks have mirrored the trend, both exhibiting gains, which is surprising given the current robust crude runs in the US.

Falling USGC freight rates and rising rates from the AG, WCI, and South Korea to South America position the US as the best to export.

Stocks

US distillate stocks are still 10 million barrels below the 10-year average, but the deficit narrowed from 18 million barrels at the start of March.

U.S. manufacturers are slowly emerging from a prolonged but shallow slowdown over the last two years.

The Institute for Supply Management's manufacturing index slipped to 48.7 in May from 49.2 in April and a recent high of 50.3 in March, the first reading above 50 since October 2022.

More than 75% of all diesel in the US is used in freight, manufacturing, and construction.

Arbs

South Korean diesel arbitrages are most competitive in Singapore.

Arbs from the Middle East (AG) and West Coast India continue to show East due to the narrow EW (East minus West differential) and the elevated AG/WCI LR2 freight rates.

USGC TA arbitrages to Europe are shut down due to the high USGC freight rates.

Flows support a continuing bearish outlook for Singapore diesel and bullish European diesel until the US/Eur arb opens.

Asian Flows

Overall, diesel exports from India, China, Singapore, and the Middle East have increased in May.

Exports from MEG have reached their highest levels since 2022, following the full start-up of new refineries in the region, but they are facing competition from Russian barrels in the South Atlantic.

References

(n.d.). US Treasuries Yield Curve. US Treasuries Yield Curve. https://www.ustreasuryyieldcurve.com/

(n.d.). CME FedWatch Tool. CME Group. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

(n.d.).Trading Economics. Trading Economics. https://tradingeconomics.com/united-states/nahb-housing-market-index

(n.d.).Goldman Sachs. Goldman Sachs. https://www.goldmansachs.com/

(n.d.).Bloomberg. Bloomberg. https://www.bloomberg.com

Disclaimer

Wizard of Soho LLC and Weekly Wizdom publish financial information based on research and opinion. We are not investment advisors, and we do not provide personalized, individualized, or tailored investment advice, nor do we provide legal advice or information. The publisher does not guarantee the accuracy of the information provided on this page. All statements and expressions present are based on the author's or paid advertiser's opinion and research. Directly or indirectly, no opinion is an offer or solicitation to buy or sell the securities or financial instruments mentioned.

As news is ever-changing, the opinions included should not be taken as specific advice on the merits of any investment decision. Investors should pursue their investigation and review of publicly available information to make decisions regarding the prospects of any company discussed. Any projections, market outlooks, or estimates herein are forward-looking and inherently unreliable. They are based on assumptions and should not be construed to be indicative of actual events that will occur.

Contrarily, other events that were not considered may occur and significantly affect the returns or performance of the securities discussed herein. The information provided is based on matters as they exist on the date of preparation and do not consider future dates. As a result, the publisher undertakes no obligation to correct, update, or revise the material in this document or provide any additional information. The publisher, its affiliates, and clients may currently or foreseeably have long or short positions in the securities of the companies mentioned herein. They may, therefore, profit from fluctuations in the trading price of the securities. There is, however, no guarantee that such persons will maintain these positions. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile, or any other means is illegal and punishable.

Neither the publisher nor its affiliates accept any liability for any direct or consequential loss arising from any use of the information contained herein. By using the website or any affiliated social media account, you consent and agree to this disclaimer and our terms of use.